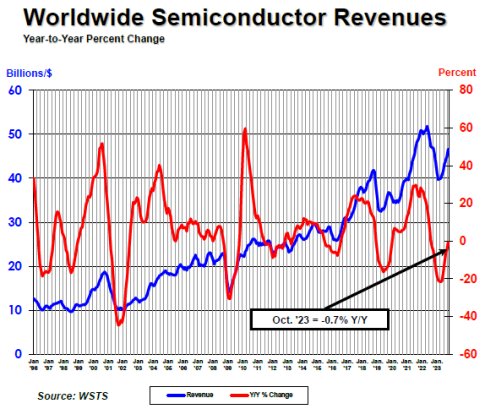

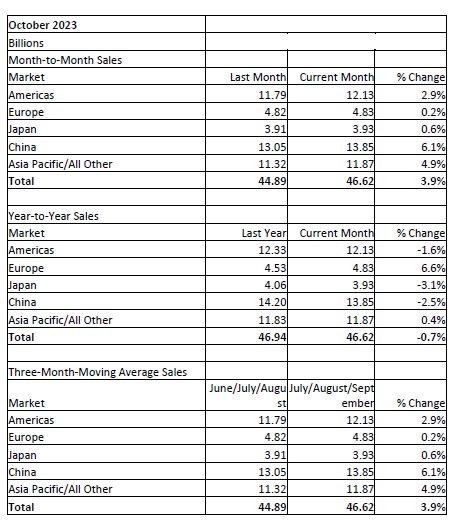

October semiconductor sales of $46.6 billion were up 3.9% on the $44.9 billion of September but 0.7% less than the October 2022 total of $46.9 billion, says the SIA.

A WSTS industry forecast projects 2023 sales will decrease 9.4% y-o-y in 2023 but increase 13.1% in 2024.

The forecast puts 2023 sales at $520 billion in 2023, down from the 2022 sales total of $574.1 billion.

In 2024, sales are projected to reach $588.4 billion.

“The global semiconductor market grew on a month-to-month basis for the eighth consecutive time in October, demonstrating clear, positive momentum for chip demand as 2023 winds down,” says SIA CEO John Neuffer, “moving forward, we forecast year-end sales for 2023 will be down compared to 2022, but the global semiconductor market is projected to rebound strongly next year with double-digit growth projected for 2024.”

Regionally, month-to-month sales increased in China (6.1%), Asia Pacific/All Other (4.9%), the Americas (2.9%), Japan (0.6%) and Europe (0.2%). Year-to-year sales were up in Europe (6.6%) and Asia Pacific/All other (0.4%), but down in the Americas (-1.6%), China (-2.5%), and Japan (-3.1%).

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

The artificial intelligence(AI) boom is triggering an unprecedented expansion race among the world's largest memory chipmakers.Surging demand for high-bandwidth memory (HBM) and high-performance D

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $298.5 billion during the first quarter of 2026, an increase of 25% compared to Q4 of 2025. Global sales we

Texas Instruments (TI) reported robust results for the first quarter of 2026 on April 23, driven by surging AI data center demand and a notable rebound in industrial control applications. TI stressed