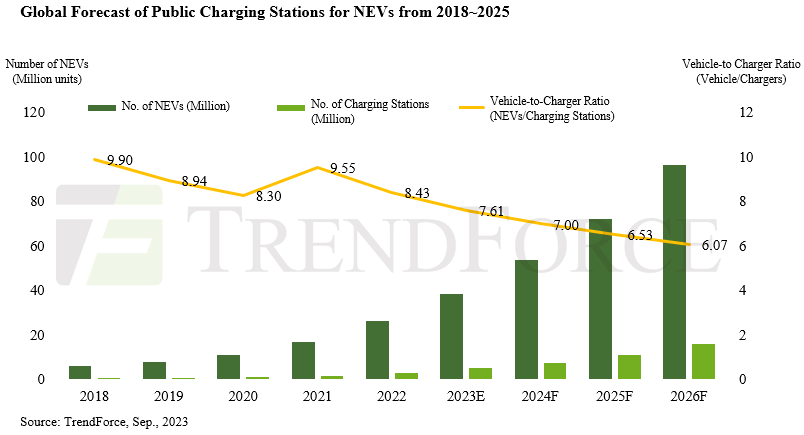

The number of EV charging stations across the world will increase 3x between 2023 and 2026 to 16 million charging points, says TrendForce.

By 2026, the number of EV’s will be 96 billion globally setting the vehicle-to-charger ratio at 6:1, a significant drop from the 10:1 ratio in 2021.

Europe is targeting the construction of 17 million charging stations by 2030.

America, with a little over 200,000 charging stations currently, aspires to hit the 500,000 mark by 2026 which will coincide with a projected EV count of 15 million, delivering a vehicle-to-charger ratio to 32:1.

Around the same period, Europe and China are projected to have ratios of approximately 9:1 and 4:1, respectively.

NEV owners globally grapple with a maze of charging standards. Prominent among these are the US standard CCS1 (Combo), the European standard CCS2 (Combo), Japan’s CHAdeMO, China’s GB/T, and Tesla’s NACS standard. Europe and China offer a simpler scenario for their citizens by adhering to a single domestic standard.

In contrast, the US is a battleground, with both CCS1 and NACS standards vying for dominance. While adapters provide a temporary bridge between the two, the rapid rise of NACS kindles apprehension among CCS1 aficionados about their future stake.

A diverse array of charging standards across the globe means charging equipment manufacturers must adopt flexible product strategies to cater to different market specifications.

GM, Mercedes-Benz, BMW, HONDA, Hyundai-Kia, and Stellantis are joining forces to spin off dedicated charging infrastructure companies.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

The artificial intelligence(AI) boom is triggering an unprecedented expansion race among the world's largest memory chipmakers.Surging demand for high-bandwidth memory (HBM) and high-performance D

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $298.5 billion during the first quarter of 2026, an increase of 25% compared to Q4 of 2025. Global sales we

Texas Instruments (TI) reported robust results for the first quarter of 2026 on April 23, driven by surging AI data center demand and a notable rebound in industrial control applications. TI stressed