Infineon Technologies expects moderate growth in fiscal 2026 as geopolitical uncertainties, tariff risks, and currency fluctuations weigh on near-term performance. CEO Jochen Hanebeck said the company remains well-positioned for long-term growth, driven by structural demand and rising opportunities in AI and energy efficiency.

Exchange rates and recovery pace temper outlook

CEO Jochen Hanebeck said unfavorable exchange rates and uncertainty around market recovery will temper fiscal 2026 growth. "We are once again setting a prudent bar with our full-year outlook," he said, citing ongoing geopolitical and tariff challenges. Despite near-term headwinds, Hanebeck emphasized Infineon's strong position to lead its markets and drive profitable long-term growth through structural demand drivers, including automotive electrification, energy efficiency, and digitalization.

December quarter revenue to fall 9%

For the December 2025 quarter—the first of fiscal 2026—Infineon forecasts revenue of around EUR3.6 billion (US$4.17 billion), assuming a US dollar-euro exchange rate of 1.15. This represents a 9% sequential decline, steeper than typical seasonality, driven by inventory reductions among automotive and industrial customers heading into year-end. Green Industrial Power (GIP) and Connected Secure Systems (CSS) are projected to decline more than average, while Automotive (ATV) and Power & Sensor Systems (PSS) should fare better.

Infineon anticipates a segment result margin in the mid-to-high teens for the quarter, reflecting lower sales volumes. Compared with the same quarter last year, nominal revenue is expected to grow 5%, or 11% on a currency-adjusted basis.

Currency shifts to drag EUR400 million off revenues

For the full fiscal year, Infineon expects moderate revenue growth from fiscal 2025 levels, though pricing pressures and a weaker US dollar will mask gains. The company estimates an approximate EUR400 million top-line headwind from exchange rate effects, assuming an average US dollar-euro rate of 1.15 versus 1.11 in fiscal 2025. It projects a fully adjusted gross margin in the low-40% range and a segment result margin in the high-teens.

Customer orders remain short-term, reflecting continued caution amid global trade and tariff uncertainties. While inventory levels have normalized across supply chains, some pockets of digestion persist alongside isolated supply constraints. "As a base case, we are expecting volume growth to return in 2026 amid a gradual upcycle," Hanebeck said.

Marvell deal weighs on cash flow

CFO Sven Schneider said free cash flow in the September 2025 quarter was affected by the acquisition of Marvell's Ethernet business, resulting in a reported outflow of EUR1.28 billion. Excluding the acquisition, free cash flow would have been positive EUR904 million. The transaction reduced the company's liquidity and leverage metrics, with a gross cash position of EUR2.1 billion at the end of September 2025—still within its liquidity target.

Infineon's fiscal 2026 outlook incorporates both upside and downside scenarios. Potential headwinds include continued tariff impacts, slower electric vehicle adoption, and escalating geopolitical tensions, while upside potential could come from stronger market recovery, higher AI-related demand, and easing inventory constraints.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

Following a record-setting year for the semiconductor industry, the start of the new year has continued the momentum, as semiconductor revenue grew 27% in 1Q26 from 4Q25 to reach US$319bn, according t

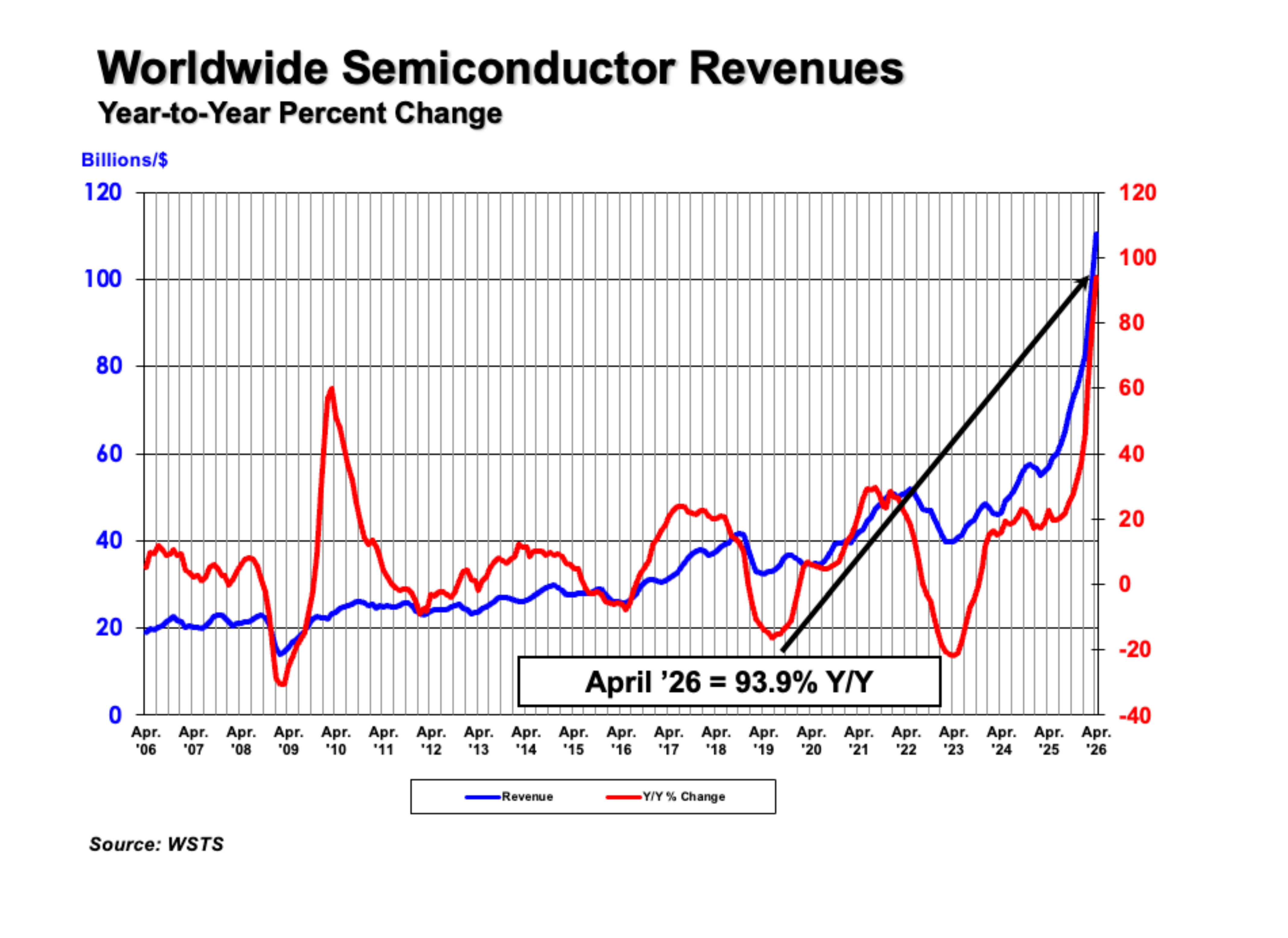

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $110.5 billion during the month of April 2026, an increase of 11% compared to the March 2026 total of $99.5

UMC held its shareholders' meeting on May 27, with CEO Jason Wang saying that as AI applications expand rapidly, long-term semiconductor demand still has room for growth. In addition to deepening