Global semiconductor sales reached $64.9 billion in August 2025, marking a remarkable 21.7% increase compared to the same period the previous year. This performance underscores the strength of a sector driven by the rise of artificial intelligence and data center infrastructure. The Asia-Pacific region and the Americas stand out as key drivers of this expansion, while Europe is cautiously beginning a recovery after several months of contraction.

Growth momentum driven by strategic geographic regions

The figures released by the Semiconductor Industry Association show that the global semiconductor market recorded sales of $64.9 billion in August 2025. This performance reflects not only an annual increase of 21.7% compared to the $53.3 billion in August 2024 but also a monthly growth of 4.4% compared to the $62.1 billion in July 2025.

This data, compiled by the World Semiconductor Trade Statistics and representing a three-month moving average, demonstrates a sustained upward trend throughout the second half of the year. John Neuffer, President of the SIA, highlighted that global semiconductor sales continued to grow in August, significantly surpassing last year's August figures, with sales in the Asia-Pacific region and the Americas continuing to drive growth. There has been notable growth in memory and logic chip sales. The geographical distribution of this expansion shows marked disparities between regions.

The Asia-Pacific region, excluding Japan and China, shows the most dramatic growth with an annual increase of 43.1%, confirming the central role of this area in the manufacturing and consumption of electronic components. The Americas follow with a growth of 25.5%, driven notably by the US market, which reached a record $232 billion over the twelve months ending in August 2025, reflecting a year-on-year increase of 44%. China registered a more moderate increase of 12.4%, while Europe, after struggling for months, returns to growth at 4.4%, marking its fifth consecutive month of annual increase after a prolonged downturn since December 2023. Japan stands out as an exception, with a decline of 6.9%, reflecting ongoing challenges in its domestic market. On a monthly basis, all regions recorded growth between July and August 2025, demonstrating the overall strength of demand.

Artificial Intelligence and Memory Chips at the Heart of Sector Dynamics

In the first half of 2025, the global semiconductor market reached $346 billion, marking an 18.9% year-over-year increase. This growth is primarily driven by two product categories that have experienced particularly significant advances. Logic chips saw a 37% growth, fueled by the massive demand for processors designed for artificial intelligence applications and data center infrastructure. Meanwhile, memory components grew by 20%, benefiting from the rise of AI servers that demand increasingly larger storage capacities. Sensors also performed well with a 16% increase, while the analog and micro segments experienced more modest growth at 4% each.

Conversely, certain segments have struggled, notably discrete components, which fell by 4%, and optoelectronics, which saw a slight decrease of 0.5%. Artificial intelligence is now emerging as the main catalyst for growth in the sector. AI applications, whether in machine learning or inference, require significant computing power and high-performance memory. This trend is expected to continue in 2025, with AI servers and dedicated chips leading market expansion, and double-digit growth likely for logic and memory targeted for AI applications, which could account for up to 30% of the sector's total revenue.

Major cloud computing players, often referred to as hyperscalers, are heavily investing in building data centers to support their services and AI initiatives. These massive investments, amounting to hundreds of billions of dollars, directly drive the demand for advanced semiconductors. According to McKinsey, between $3.7 trillion and $5.2 trillion will be needed by 2030 for global data centers to meet the computing power demand for AI, including hardware, processors, memory, storage, and energy.

Encouraging Outlook Despite Ongoing Geopolitical Tensions

Forecasts for the entire year of 2025 have been revised upwards. The World Semiconductor Trade Statistics now projects a global market of $728 billion, reflecting an annual growth of 15.4%, a 4 percentage point increase from previous estimates. This revision is based on first-half results that exceeded expectations. For 2026, growth is expected to continue at a rate of 9.9%, bringing the market to $800 billion.

All product segments have seen upward revisions, with logic chips and memory now anticipated to grow by 29% and 17%, respectively, an improvement of 5 percentage points for each segment. Regionally, all major geographic areas are expected to expand, with the Americas and Asia-Pacific continuing to lead growth, while Europe is projected to gradually strengthen, and Japan may experience a slight decline. These optimistic prospects should not overshadow the challenges facing the industry. Geopolitical tensions between the United States and China continue to impact supply chains.

In August 2025, the Trump administration announced plans to tax semiconductors, raising questions about exemptions for companies manufacturing in the United States and the impact of such measures on American competitiveness. A US congressional report published in October 2025 revealed that five major semiconductor equipment manufacturers, including European ASML and Japan's Tokyo Electron, had sold $38 billion worth of critical technologies to China in 2024, including to companies considered a threat to US security. These developments illustrate the strategic dimension the semiconductor sector has now taken on, beyond mere economic considerations. Despite these uncertainties, the industry remains confident in its ability to maintain a strong growth trajectory, driven by the widespread adoption of artificial intelligence and the ongoing digital transformation across all sectors of the global economy.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

Following a record-setting year for the semiconductor industry, the start of the new year has continued the momentum, as semiconductor revenue grew 27% in 1Q26 from 4Q25 to reach US$319bn, according t

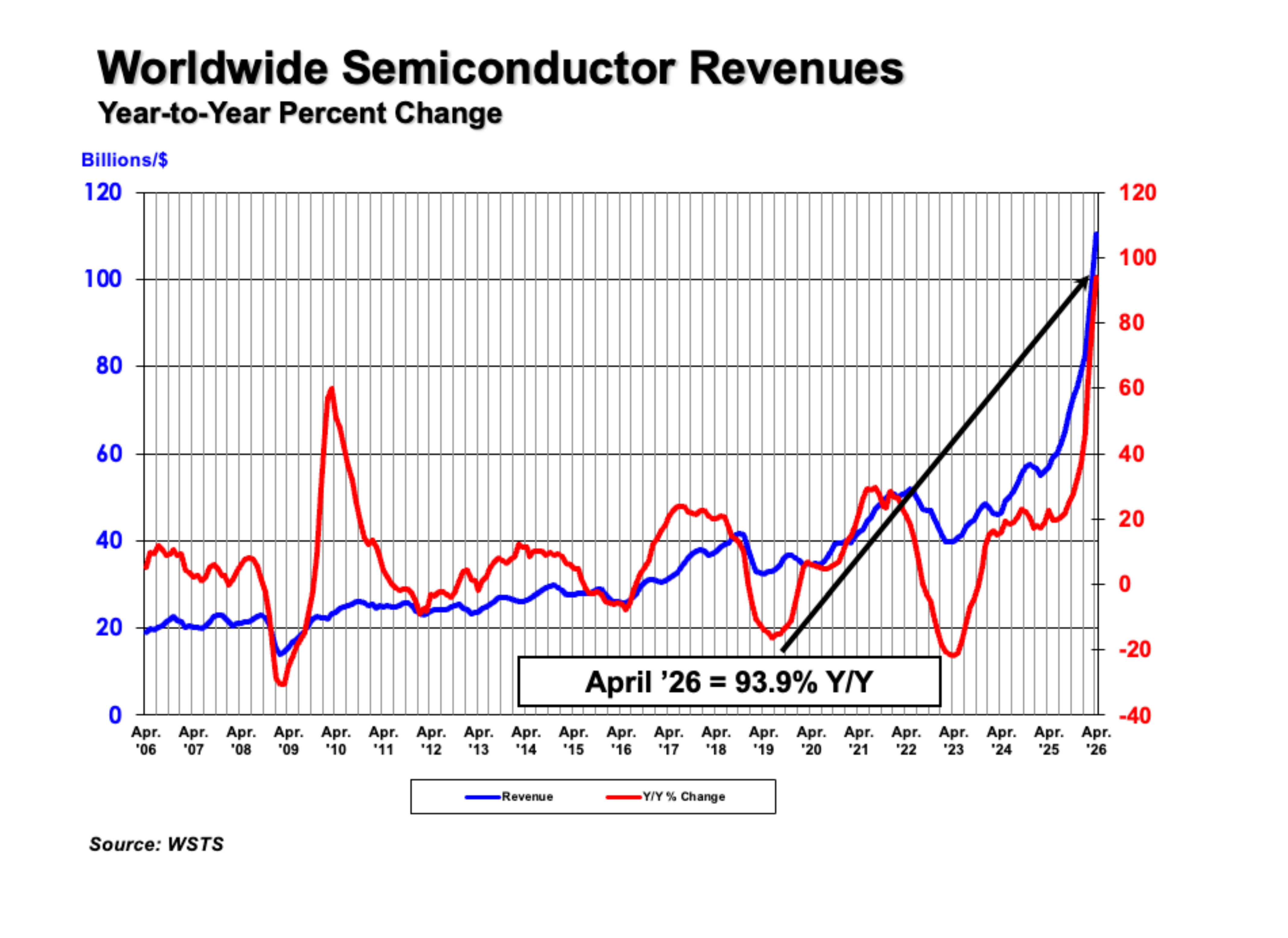

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $110.5 billion during the month of April 2026, an increase of 11% compared to the March 2026 total of $99.5

UMC held its shareholders' meeting on May 27, with CEO Jason Wang saying that as AI applications expand rapidly, long-term semiconductor demand still has room for growth. In addition to deepening