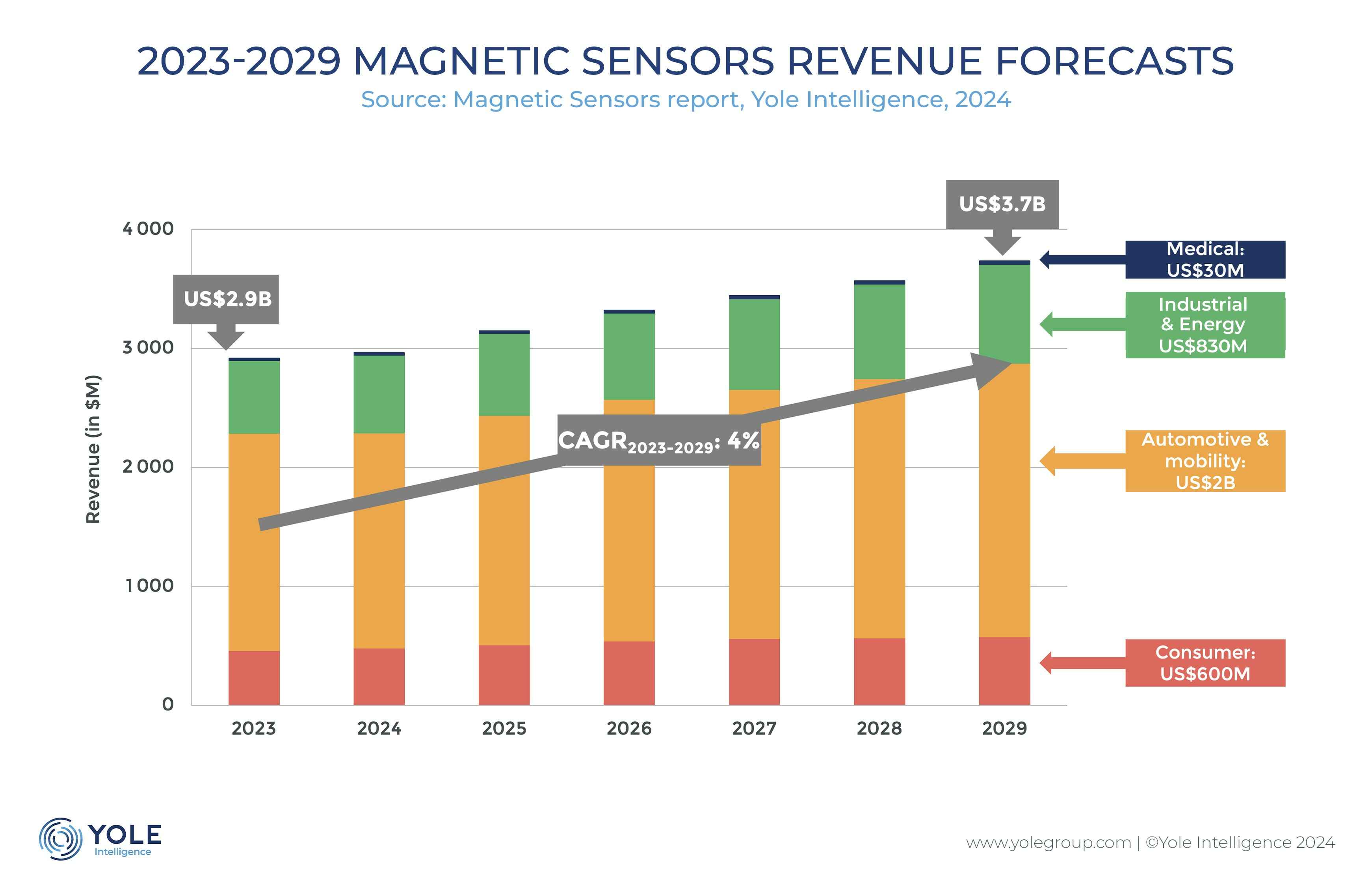

The magnetic sensor market is expected to reach $3.7 billion in 2029, with an estimated 4% CAGR from 2023 to 2029, says Yole Developpement.

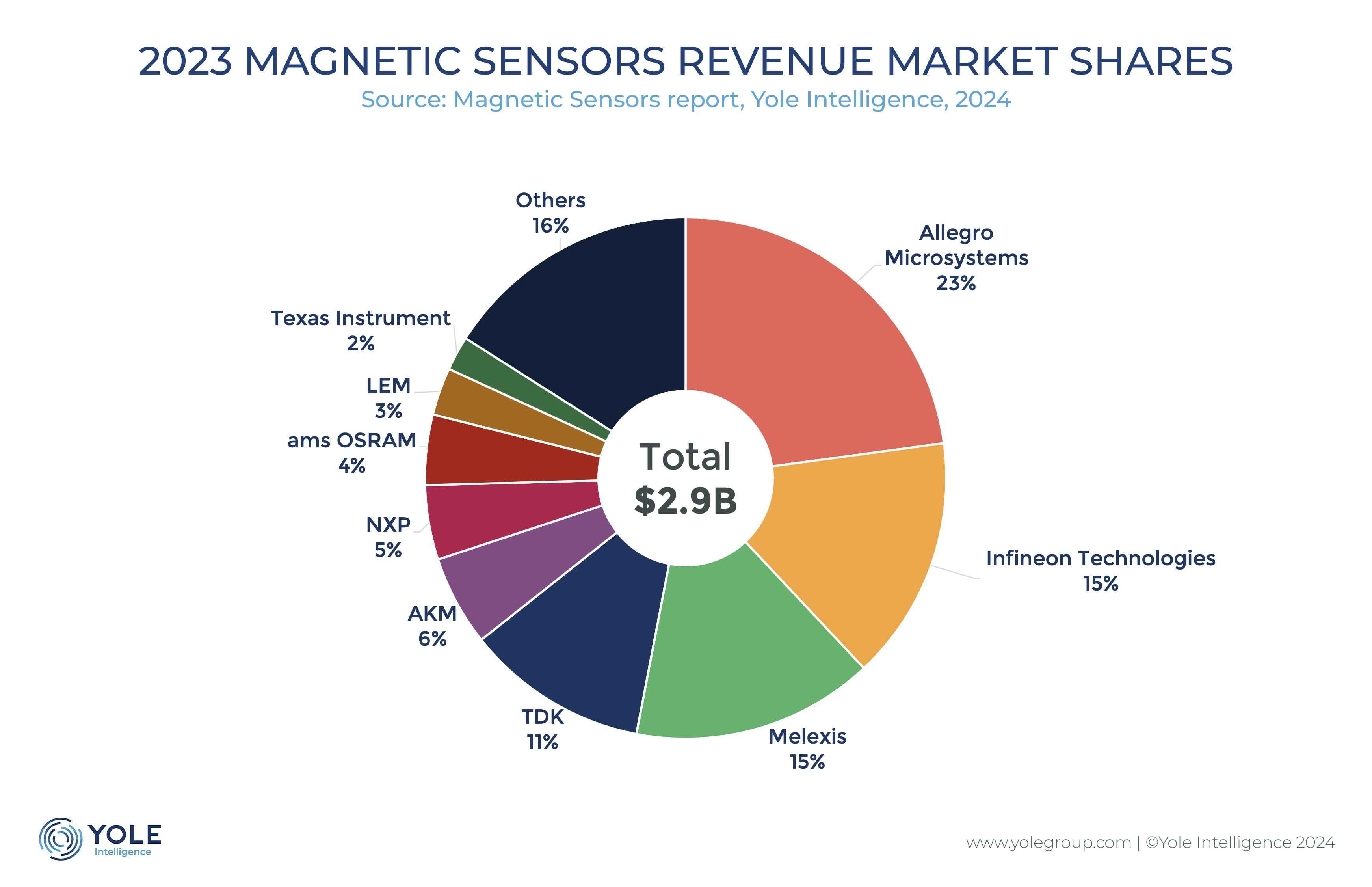

RECOMMENDED ARTICLESHBM to be 14% of DRAM industry this yearUS strategy for microelectronics research publishedTelecom equipment sales fell 5% in 2023, set to fall again in 2024Smartphones bounce backAllegro Microsystems leads in revenue, TDK leads in volume.

A $1 billion investment surge from players like Allegro, TDK, Bosch, LEM etc. is leveraging the technology’s sensitivity, bandwidth, and low power consumption to sense position and current.

Magnetic sensors find widespread application across automotive, mobility, industrial, energy, medical, and consumer sectors. Their versatility has led to their adoption in various fields, propelling the market to a value of $2.9 billion in 2023.

“The automotive & mobility segment significantly dominates the market with sales of more than $2 billion by 2029,” says Yole’s Pierre Delbos, “this segment is driven by important shifts such as vehicle electrification and sensor integration. Conversely, consumer applications lead in terms of volume. At Yole Group, we anticipate a nearly $600 million market by 2029, also growing at a 4% CAGR between 2023 and 2029”.

The evolving landscape of magnetic sensor applications extends to the industrial & energy and medical sectors. By 2029, these sectors are expected to reach $830 million and $30 million, respectively.

Factors such as the proliferation of DC-charging stations with integrated current sensors due to vehicle electrification, the demand for position sensors, switches, and latches driven by Industry 4.0, and the potential implementation of predictive maintenance using current sensors contribute to the promising outlook in these sectors.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

The artificial intelligence(AI) boom is triggering an unprecedented expansion race among the world's largest memory chipmakers.Surging demand for high-bandwidth memory (HBM) and high-performance D

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $298.5 billion during the first quarter of 2026, an increase of 25% compared to Q4 of 2025. Global sales we

Texas Instruments (TI) reported robust results for the first quarter of 2026 on April 23, driven by surging AI data center demand and a notable rebound in industrial control applications. TI stressed