Q4 is expected to see a further 5–10% QoQ increase in production.

The downturn in global smartphone production for 2023 is expected to be limited to less than 3%, with total annual output estimated to reach approximately 1.16 billion units.

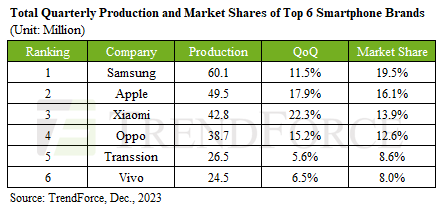

Samsung continues to lead the market after recording an 11.5% increase in its Q3 production at 60.1 million units – only 5 million more than apple.

Apple saw its Q3 production climb 17.9% to reach approximately 49.5 million units. However, it had a 1.5% YoY market share decline, with annual production at 2022 levels.

Huawei’s re-entry with its flagship phones is anticipated to significantly impact Apple’s production performance in the upcoming year.

Xiaomi (including Xiaomi, Redmi, and POCO) saw Q3 production jump by 22.3% to approximately 42.8 million units.

Oppo (including Oppo, Realme, and OnePlus) experienced a 15.2% increase in its Q3 output to 38.7 million units.

Transsion (including TECNO, Infinix, and itel) produced 26.5 million units—a 5.6% increase QoQ.

Vivo (including Vivo and iQoo) saw its Q3 production rise to 24.5 million units, marking a 6.5% increase and placing it in the sixth spot.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

The artificial intelligence(AI) boom is triggering an unprecedented expansion race among the world's largest memory chipmakers.Surging demand for high-bandwidth memory (HBM) and high-performance D

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $298.5 billion during the first quarter of 2026, an increase of 25% compared to Q4 of 2025. Global sales we

Texas Instruments (TI) reported robust results for the first quarter of 2026 on April 23, driven by surging AI data center demand and a notable rebound in industrial control applications. TI stressed