The artificial intelligence(AI) boom is triggering an unprecedented expansion race among the world's largest memory chipmakers.

Surging demand for high-bandwidth memory (HBM) and high-performance DRAM used in AI servers is pushing Samsung Electronics and SK Hynix to accelerate factory construction, equipment orders, and production timelines at a pace rarely seen in the memory industry.

According to industry reports cited by South Korean media outlet Ddaily, both companies have significantly revised their investment plans to secure next-generation DRAM capacity ahead of an expected multiyear AI infrastructure boom. The companies are reportedly moving up fab ramp schedules and committing billions of dollars in new spending, setting the stage for a major wave of semiconductor equipment demand.

Industry executives say the shift reflects more than a conventional battle for market share.

As AI models become increasingly sophisticated, the amount of memory required inside each server is growing exponentially. That has transformed memory capacity into a critical bottleneck for the broader AI industry, making aggressive expansion a matter not only of competitiveness, but long-term survival.

HBM production is especially demanding. Compared with conventional DRAM, HBM chips use larger die sizes and require more complex yield management. Producing the same volume of HBM can consume two to three times more wafer capacity than standard DRAM. At the same time, manufacturers are transitioning toward more advanced process technologies, including fifth-generation 10nm class DRAM and sixth-generation 1c DRAM, both of which naturally reduce effective output during migration.

Without substantial new fabrication capacity, industry analysts warn that suppliers may struggle to meet the explosive rise in AI-related demand.

Samsung

Samsung has recently accelerated DRAM investment at its Pyeongtaek P4 campus, one of its core semiconductor manufacturing hubs. Equipment installation at the facility has reportedly advanced faster than expected, with upper-floor production lines scheduled to complete front-end equipment setup by the second half of 2026.

The moves suggest Samsung is abandoning the more conservative capital spending posture it adopted during the previous memory downturn and shifting aggressively back into expansion mode.

Some market estimates now project Samsung's DRAM capacity additions in 2027 could exceed prior expectations by roughly 10,000 wafers per month. Industry observers also expect Samsung to begin procurement orders for its next major Pyeongtaek P5 facility as early as the second quarter of 2027, with annual investments potentially reaching 150,000 wafers of capacity expansion that year.

The company's broader goal is to reclaim leadership in the HBM market while expanding its share of high-capacity DDR5 memory modules used in AI servers and data centers.

SK Hynix

SK Hynix is also accelerating expansion plans at its Cheongju M15X and Yongin Y1 facilities. Analysts expect the company's DRAM-related capital expenditures in 2027 to roughly double from 2026 levels.

The M15X fab in Cheongju, originally intended for NAND flash production, is now being converted into a DRAM manufacturing base, with equipment installation timelines reportedly being pushed forward as aggressively as possible.

With NAND demand beginning to recover and AI memory pricing strengthening, SK Hynix is moving at what industry executives describe as an unprecedented pace. The M15X facility is expected to become a key production hub for next-generation through-silicon via (TSV) technology used in advanced HBM packaging, potentially triggering another wave of front-end and back-end semiconductor equipment orders.

At the same time, expanding investment in AI servers is steadily increasing the baseline demand for memory across the broader data center industry.

According to South Korean outlet Newdaily, analysts at Hana Securities said recent growth trends in server CPUs from AMD and Intel suggest memory consumption in servers and data centers is likely to continue rising alongside processor upgrades.

Recent pricing trends appear to reinforce that view. Data from Kiwoom Securities showed average PC DRAM prices in April 2026 rose 26% from the previous month, while server DRAM prices increased 4%.

As AI servers require dramatically larger amounts of memory and storage than conventional computing systems, analysts expect the profitability foundation for both Samsung and SK Hynix to strengthen alongside the industry's accelerating investment cycle.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

Following a record-setting year for the semiconductor industry, the start of the new year has continued the momentum, as semiconductor revenue grew 27% in 1Q26 from 4Q25 to reach US$319bn, according t

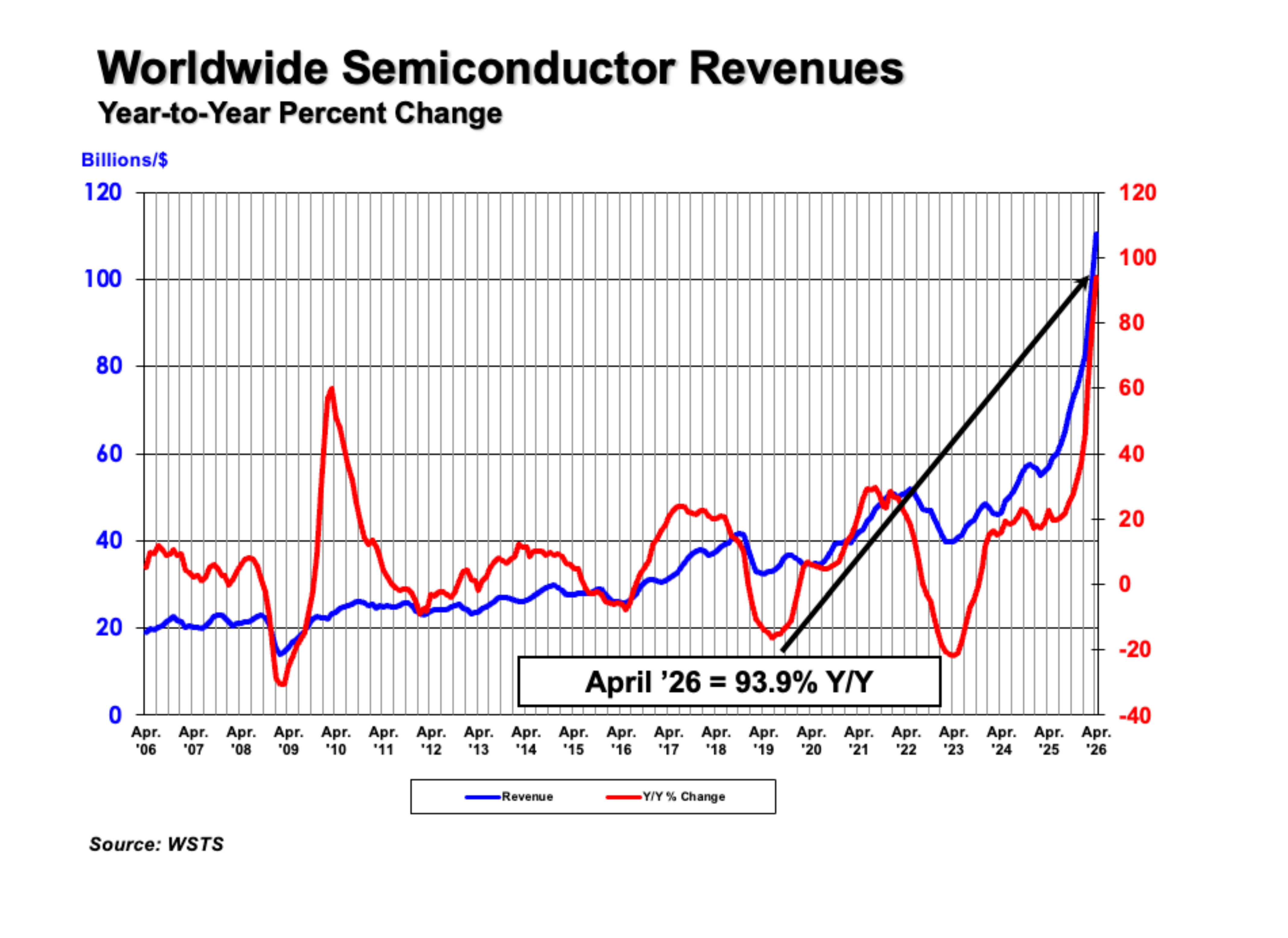

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $110.5 billion during the month of April 2026, an increase of 11% compared to the March 2026 total of $99.5

UMC held its shareholders' meeting on May 27, with CEO Jason Wang saying that as AI applications expand rapidly, long-term semiconductor demand still has room for growth. In addition to deepening