According to supply chain sources, memory contract prices are expected to increase significantly over the coming quarters, with gains likely to exceed previous market expectations.

Reports indicate that contract pricing for the third quarter of 2026 is still under negotiation. While the market had previously anticipated a moderation in price increases due to the high base established in earlier quarters, supply chain sources now suggest that both DRAM and NAND Flash contract prices are likely to rise far more sharply than originally forecast. DDR5 prices have already begun to climb, while legacy DDR4 products are also expected to see substantial increases. In particular, 8Gb DDR4 contract prices are projected to surge by more than 50% during the third quarter.

Industry sources attribute the tightening market primarily to the rapid growth in enterprise SSD demand driven by AI applications. As enterprise storage deployments continue to expand, the supply-demand gap for 8Gb DDR4 DRAM is expected to widen further, with shortages potentially lasting for as long as two years.

Spot prices for 16Gb DDR4 have already reached elevated levels, with certain configurations now trading at prices above comparable DDR5 products. This is largely because DDR4 remains widely used in the PC market. Amid relatively weak end-user demand, many PC manufacturers continue to rely on DDR4 platforms to maintain the competitiveness of cost-sensitive product lines.

Demand for DDR4 rebounded significantly during the second quarter of 2026, driving prices beyond earlier market forecasts. Market sources indicate that DDR4 products manufactured by Taiwanese suppliers are now being priced noticeably higher than comparable products from Samsung. Meanwhile, Samsung continues to accelerate its transition toward DDR5 and next-generation high-end memory products to increase revenue from AI-related customers.

Enterprise SSDs have also become an important driver of DDR4 demand. Although DRAM-less SSD solutions have gained market share, SSDs equipped with DRAM continue to offer clear advantages in latency reduction, cache performance, and read/write speeds. As data center storage capacity continues to expand, demand for DRAM in high-capacity SSDs is increasing accordingly. Samsung has recently introduced a 16TB PCIe 6.0 SSD designed for data center applications, while other manufacturers are also accelerating the development of next-generation storage solutions targeting AI workloads.

Currently, most DDR4 production capacity is concentrated at Nanya Technology and Winbond. As leading memory manufacturers—including SK hynix, Micron, and Samsung—continue shifting production toward high-end memory products, only limited capacity remains for legacy DRAM manufacturing. As a result, global DDR4 supply has fallen well below market demand. At the same time, manufacturers focusing on DDR4 production have also reduced capacity allocated to DDR3, further tightening supply.

As the supply-demand imbalance continues to widen, prices for legacy memory products, including DDR3, have also begun to rise. Industry analysts expect prices for 4Gb DDR4 and DDR3 products to continue increasing throughout the second half of 2026.

Market observers believe that DRAM prices—including DDR5, DDR4, and DDR3—will remain on an upward trajectory until supply shortages ease. Current expectations suggest that shortages could persist through 2028, with additional price increases likely in the fourth quarter of 2026 and an even tighter supply environment anticipated in 2027.

Stay up to date with the latest in industry offers by subscribing us. Our newsletter is your key to receiving expert tips.

Following a record-setting year for the semiconductor industry, the start of the new year has continued the momentum, as semiconductor revenue grew 27% in 1Q26 from 4Q25 to reach US$319bn, according t

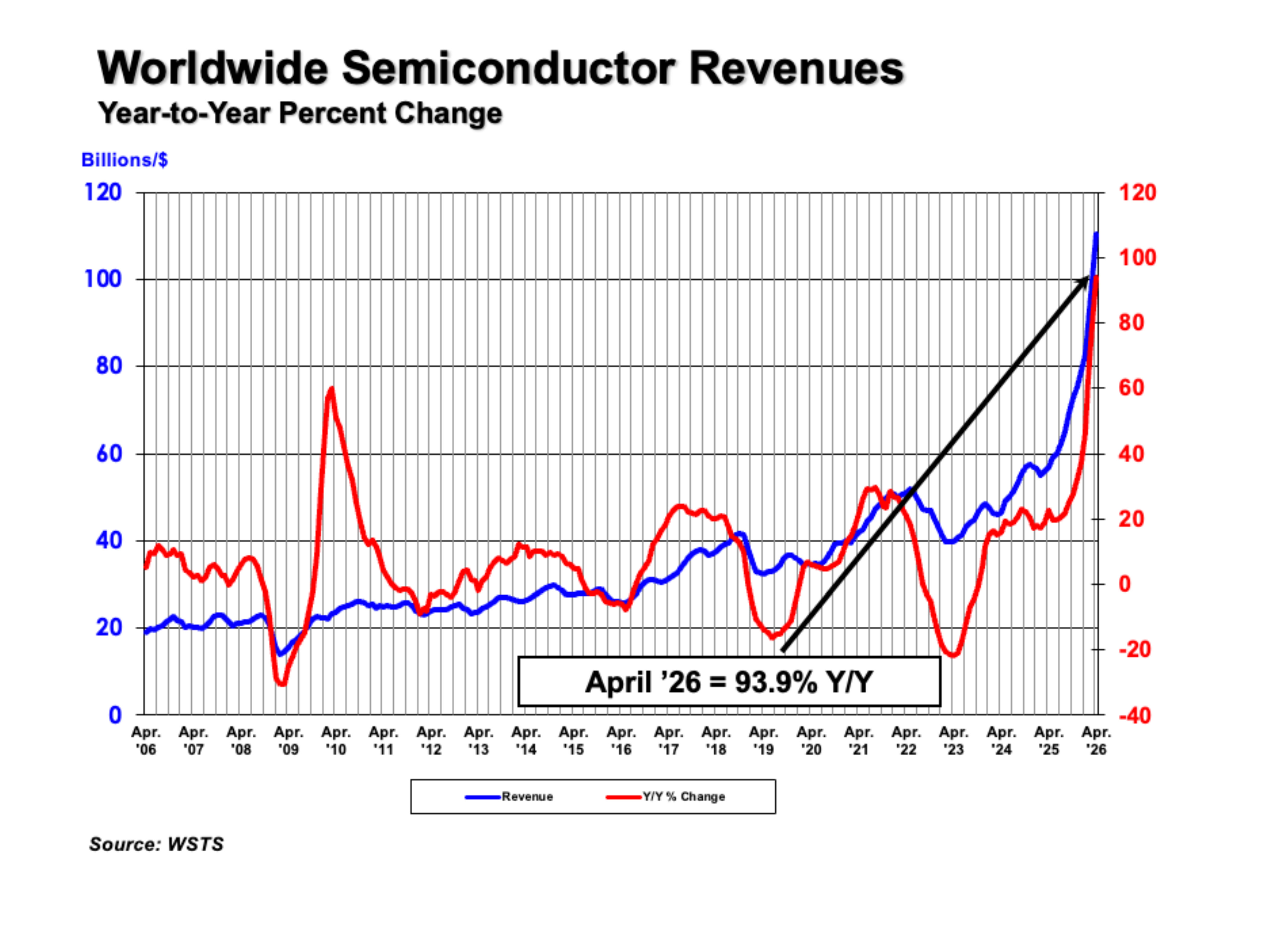

The Semiconductor Industry Association (SIA) today announced global semiconductor sales were $110.5 billion during the month of April 2026, an increase of 11% compared to the March 2026 total of $99.5

UMC held its shareholders' meeting on May 27, with CEO Jason Wang saying that as AI applications expand rapidly, long-term semiconductor demand still has room for growth. In addition to deepening